The corporate card used to be a static payment credential operating within a predetermined programme. AI is now transforming it into a programmable interface through which payment, risk, and spend decisions can be made in real time.

For most of its history, the corporate card has been a relatively simple instrument. It carried a limit, enforced a policy, and settled on a fixed rail. What happened between swipe and statement was largely invisible to the finance team that issued it. That model is changing and for global businesses managing complex, high-volume cross-border payments, the change is significant.

AI is not just being added to corporate card products as a reporting or fraud layer. In the most advanced implementations, it is becoming the decision engine that determines how, when, and through which channel a payment moves. That distinction between AI as an insight tool and AI as a transaction-level decision-maker, is the defining product question in B2B payments right now.

Reason #1: The corporate card is no longer a rail — it's a router

The traditional corporate card was optimised for a single function: authorising spend against a predefined policy. It sat on a fixed network, settled on a fixed timeline, and generated data that finance teams reviewed after the fact. The card was, in essence, a rail with a limit attached. The AI-powered corporate card operates differently. Rather than routing every transaction the same way, it functions as a dynamic payment interface which is one that can evaluate each transaction on its own terms and direct it accordingly.

The question it answers is not just "is this payment approved?" but "what is the optimal way to execute this payment, right now, given the corridor, the currency, the counterparty, and the cost?" This shift has a structural implication for product teams.

Structural Implication for Product Teams

• The Current Fragmentation: Many B2B fintech organisations still treat routing logic and card products as separate roadmap workstreams:

⇒ One team optimises for network economics

⇒ Another team optimises for cardholder experience.

• The AI Shift: The AI-powered card collapses this distinction. Thus, routing and card issuance are no longer two products, but one unified surface.

• The Risk: Teams that continue to treat them separately risk delivering a fragmented user experience.

• The Competitive Reality: Meanwhile, competitors that unify these functions will present a seamless, cohesive offering to the market.

Reason #2: AI Optimises Every Payment, Not Just Every Approval

Payment method selection has traditionally been governed by standing treasury policies, supplier setup, and predefined operational rules. A supplier was onboarded to a particular payment method, and that method was used consistently regardless of whether it remained the most efficient or cost-effective option over time.

Why Static Logic Fails in Today's Environment

That static logic is increasingly difficult to defend. Local rails are cheaper than SWIFT in most corridors and settle same-day or instantly compared to the one-to-three-day timelines of traditional correspondent banking.

Yet most corporate card products still route to a single predetermined rail, offering buyers no visibility into whether they are getting the optimal path, or quietly absorbing the cost of one that has fallen behind.

The AI-Driven Solution

• An AI-driven system evaluates each transaction dynamically, selecting the best combination of:

⇒ Processor – which intermediary to use

⇒ Rail – which network (e.g., local ACH, SWIFT, card network)

⇒ FX Path – which foreign exchange route minimizes conversion costs

• Decision Criteria: The scoring model weighs three core factors per transaction:

⇒ Cost (fees and FX spreads)

⇒ Settlement speed (time to funds receipt)

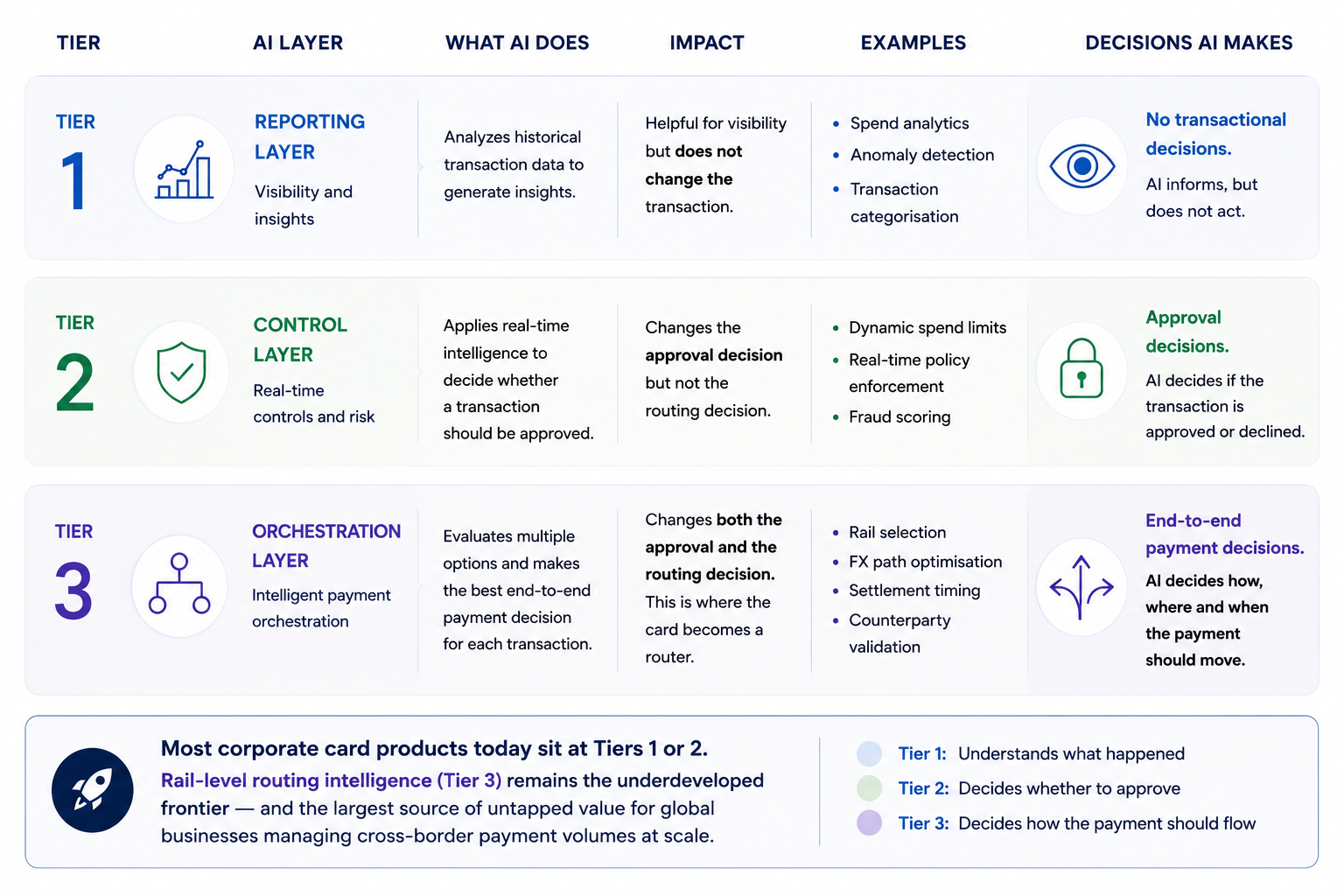

Reason #3: Truly AI-Powered Cards Go Beyond Analytics

"AI-powered" is rapidly becoming the most overloaded term in B2B fintech. Nearly every card product now claims some form of AI capability, which makes it harder to distinguish meaningful differentiation from marketing positioning. For product teams and buyers, the distinction that matters is not whether AI is present, but what decisions it is actually making. A useful way to think about this is in tiers.

Reason #4: Virtual Cards Are the Ideal Interface for AI

If the AI-powered card is a router, the virtual card is its most natural form factor. Single-use, programmable, and issuable at the transaction level, virtual cards are structurally suited to per-payment configuration in a way that physical cards are not. Most virtual card issuance today, however, is still rule-based.

A card is created for a vendor, assigned a limit, and settled on whatever rail the issuer defaults to. The AI opportunity sits in replacing that standing configuration with a dynamic one, where the system determines at the point of payment whether a virtual card is the most appropriate method, and if so, issues the credential with transaction-specific settings based on corridor, amount, currency, timing, supplier profile, and policy requirements.

The industry is already taking steps in this direction. Visa's work with enterprise platforms such as Ramp is moving towards AI agent-initiated corporate spending, where trusted AI agents can execute business purchases within predefined policies and spending limits. Rather than relying solely on conventional employee cards, the focus is shifting towards identity-bound payment credentials and delegated authority for AI agents. This is an important step towards agent-native corporate spending.

Reason #5: Intelligent Routing Requires Intelligent Compliance

Routing intelligence without compliance intelligence is not a feature but a liability. In cross-border B2B payments, the optimal rail and the compliant rail are not always the same rail, and the decision about which to use must account for both dimensions simultaneously.

Before processing cross-border payments, regulated institutions must apply sanctions screening, AML and CFT controls, customer due diligence, and transaction monitoring in line with their regulatory obligations.

Whether a payment is routed via SWIFT, local clearing networks or other payment methods, equivalent compliance controls must be applied. These decisions cannot be evaluated separately across different systems as they need to be resolved within a single decisioning layer at the point of payment.

This is where card networks provide an advantage beyond standalone routing logic. Credential controls, tokenisation, issuer oversight and established dispute mechanisms create an additional layer of trust and security.

As agentic payment protocols begin embedding identity and authorisation directly into payment workflows, card products that integrate with these protocols inherit stronger trust signals, strengthening not only routing intelligence, but the overall compliance and governance framework.

What B2B fintech product teams should build next

The key question for B2B fintech teams is not whether to add AI to corporate cards, but whether payment routing and card products are designed as a single intelligent experience. Teams that invest early in AI-powered routing will build a compounding data advantage, using insights from payment performance, FX outcomes and settlement success to continuously improve decision-making.

Corporate cards spent decades as a spending instrument. As demand grows for connected, real-time payment experiences, corporate cards are evolving beyond spend management into intelligent interfaces that orchestrate payments across multiple rails—including SWIFT, local clearing networks and real-time payment systems—through a unified platform.

Its next chapter is as a payment intelligence layer. The teams that recognise that shift earliest will be the ones that define what the category looks like on the other side of it.

To get started and partner with a solutions provider that can help your business optimise payments and help you scale both locally and globally, open a SUNRATE account today or contact our sales team.

Share to

The corporate card used to be a static payment credential operating within a predetermined programme. AI is now transforming it into a programmable interface through which payment, risk, and spend decisions can be made in real time. For most of its history, the corporate card has been a relatively simple instrument. It carried a […]

Every major technology vendor serving the finance industry is selling AI. AI-powered forecasting. AI-driven compliance. Autonomous treasury management. Intelligent payment routing. The capability announcements are impressive, the demos are compelling, and the ROI projections are substantial. And yet, across organisations that have invested in AI for their finance functions, a consistent pattern is emerging: […]

B2B payment fraud has grown more sophisticated, more automated, and more difficult to catch with traditional safeguards. Passwords get phished, one-time codes get intercepted, and approval workflows built around email and static credentials are increasingly exposed to business email compromise and synthetic identity fraud. In response, biometric authentication, which was once associated mainly with unlocking a smartphone, is becoming […]

We hope to use cookies to better understand your use of this website. This will help improve your future experience of accessing this website. For detailed information on the use of cookies and how to revoke or manage your consent, please refer to our < privacy policy >. If you click the confirmation button on the right, you will be deemed to have agreed to use cookies.