Choosing a payment gateway is rarely the hard part. Choosing how to integrate it — and making sure that integration fits your technical resources, your customer experience goals, and your growth ambitions — is where most businesses spend too little time and pay for it later.

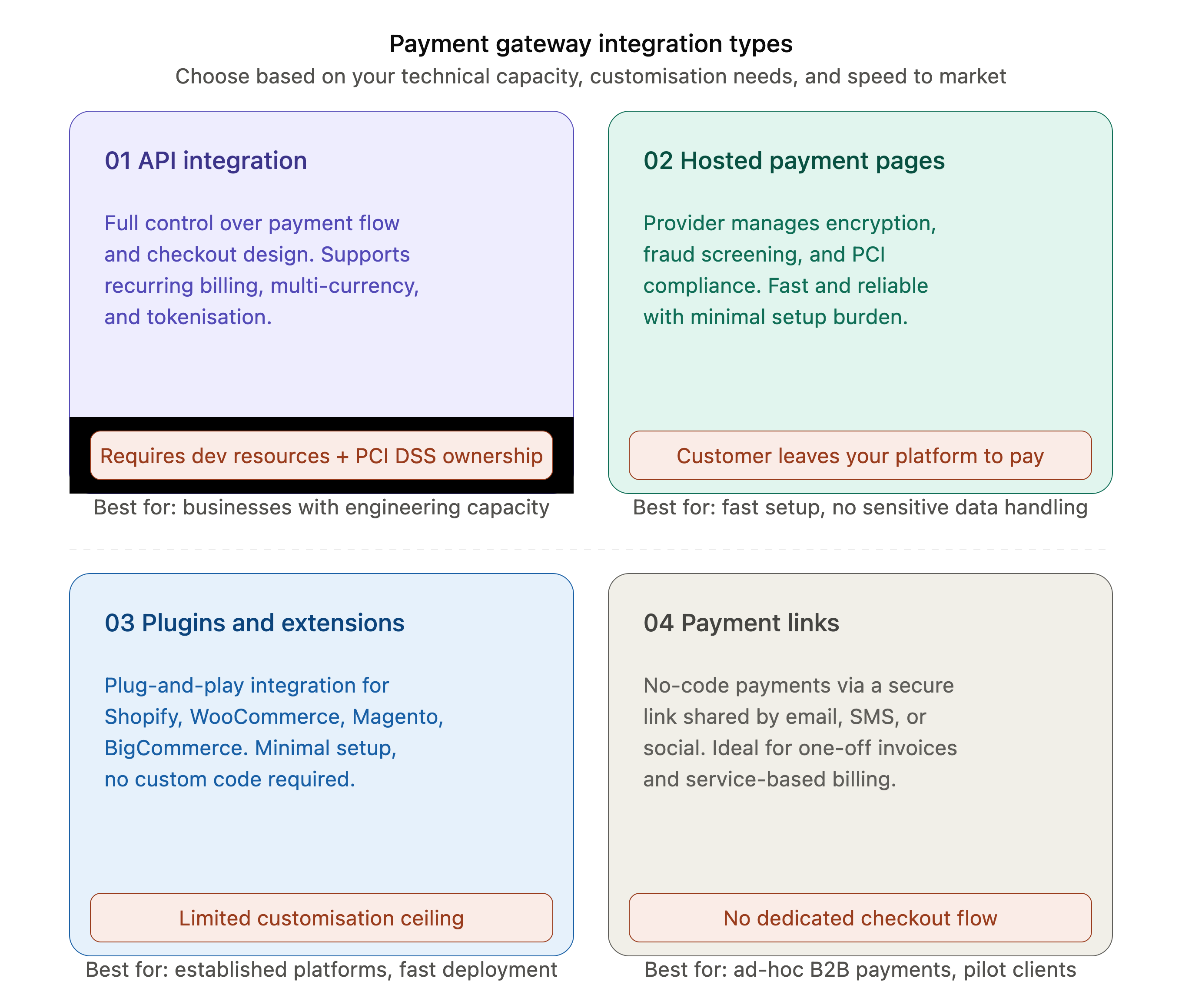

Understanding the integration options

Every payment gateway offers more than one way to connect. The method you choose shapes how much control you have over the checkout experience, how quickly you can get up and running, and how much of the security and compliance burden sits with your team.

What good gateway integration actually delivers

The right integration does more than process payments. It has a measurable impact on conversion, cost, and operational efficiency.

• Broader payment method coverage reduces abandonment

B2B buyers increasingly expect to pay through methods that suit their own internal processes — bank transfers, digital wallets, and in certain markets, local payment rails that are the default for that geography. When those options are absent at checkout, transactions stall. Research consistently shows that a significant share of buyers will abandon a purchase rather than adapt to a payment method that does not fit their workflow. A gateway with broad payment method support across the markets you operate in removes that friction before it costs you a transaction.

• Multi-currency settlement reduces FX drag

For businesses receiving international payments, the cost of automatic currency conversion is one of the more persistent and underappreciated margin leaks. When every foreign currency payment is converted into your home currency at the point of receipt, you are paying a conversion cost on every transaction — often at rates that are less favourable than what a deliberate FX strategy would achieve.

Gateways that support multi-currency settlement allow you to receive and hold funds in the currency they arrive in, convert when the timing is right, and pay outbound in local currency where possible. Over meaningful payment volumes, the difference between automatic conversion and deliberate multi-currency management is significant.

• Built-in security reduces both fraud loss and false declines

A well-integrated gateway provides encryption, tokenisation, and fraud detection as standard. Tokenisation is worth understanding specifically: rather than storing or transmitting actual card numbers, the system substitutes a unique token that has no value outside the specific payment context it was created for. Even if intercepted, it cannot be used to initiate a different transaction or access account data.

Combined with 3D Secure authentication and AI-driven fraud screening, a modern gateway can reduce fraudulent transaction approvals while also reducing the rate of false declines — legitimate transactions that are incorrectly flagged and rejected. Both matter: fraud creates direct financial loss, but false declines also damage customer relationships and revenue, particularly in B2B contexts where declined payments on legitimate invoices create real operational disruption.

• Faster checkout reduces drop-off

In B2B as much as in consumer commerce, checkout friction has a measurable cost. Saved payment credentials, auto-populated fields, and mobile-optimised flows reduce the time and effort required to complete a payment. For subscription and recurring billing arrangements, where the customer should not need to re-enter payment details for every renewal, gateway support for automated recurring billing reduces churn and removes a common point of payment failure.

What to evaluate before choosing a provider

Integration fit with your existing stack

A gateway that requires extensive custom development to connect with your ERP, accounting software, or CRM creates hidden cost and delay. Assess not just the gateway's API documentation, but how it connects to the systems your finance and operations teams already rely on. The technical lift of integration is rarely the headline number — it is what emerges during and after deployment.

PSP versus dedicated merchant account

All-in-one payment service providers bundle the gateway, processor, and merchant account into a single arrangement. Setup is fast, ongoing management is lower, and the pricing is predictable. A dedicated merchant account, by contrast, involves separate relationships with an acquiring bank and gateway provider — more configuration, but potentially more control over processing terms and pricing as transaction volumes scale. For most growing B2B businesses, a PSP is the right starting point.

Security and compliance coverage

PCI DSS compliance, GDPR alignment, and data localisation requirements in key markets are not optional considerations. Evaluate providers on whether compliance coverage is built into the integration or requires additional configuration on your side — and what that means for your team's ongoing obligations.

Total cost, including FX and reconciliation

Setup fees and transaction costs are visible. Currency conversion costs, chargeback fees, and the operational overhead of manual reconciliation are less so. Evaluate the total cost of ownership across all of these dimensions, not just the headline processing rate. Automated reconciliation and real-time transaction reporting reduce finance team overhead and make it easier to identify where payment costs are accumulating.

Scalability across markets

If international expansion is part of your roadmap, your gateway needs to support it without requiring a separate integration for each new market. Multi-currency account support, local acquiring relationships, and the ability to surface region-appropriate payment methods at checkout are all capabilities worth assessing before you need them rather than after.

Choosing for where you are going, not just where you are

The best payment gateway integration for your business today may not be the right one for the business you are building toward. API integration scales with complexity; hosted pages and plugins are faster to deploy but have defined ceilings. The right choice is the one that fits your current technical capacity and experience requirements — while leaving room to add capability as your payment volumes, geographic reach, and customer expectations grow.

To get started and partner with a solutions provider that can help your business optimise payments and help you scale both locally and globally, open a SUNRATE account today or contact our sales team.

Share to

Choosing a payment gateway is rarely the hard part. Choosing how to integrate it — and making sure that integration fits your technical resources, your customer experience goals, and your growth ambitions — is where most businesses spend too little time and pay for it later. Understanding the integration options Every payment gateway offers […]

The travel industry operates on margins that leave almost no room for error. An online travel agency processing millions of transactions annually cannot treat payment failure rates as an acceptable operational variable. A hotel group with properties across twelve countries cannot manage treasury as an afterthought and expect its finance function to keep pace with the commercial operation […]

Double conversion is one of the most common and least visible sources of FX cost in cross-border payments. It happens quietly, often without the finance team realising it, and its impact compounds across every transaction that flows through a payment corridor where it occurs. What the double conversion trap actually is Double conversion occurs when a cross-border […]

We hope to use cookies to better understand your use of this website. This will help improve your future experience of accessing this website. For detailed information on the use of cookies and how to revoke or manage your consent, please refer to our < privacy policy >. If you click the confirmation button on the right, you will be deemed to have agreed to use cookies.