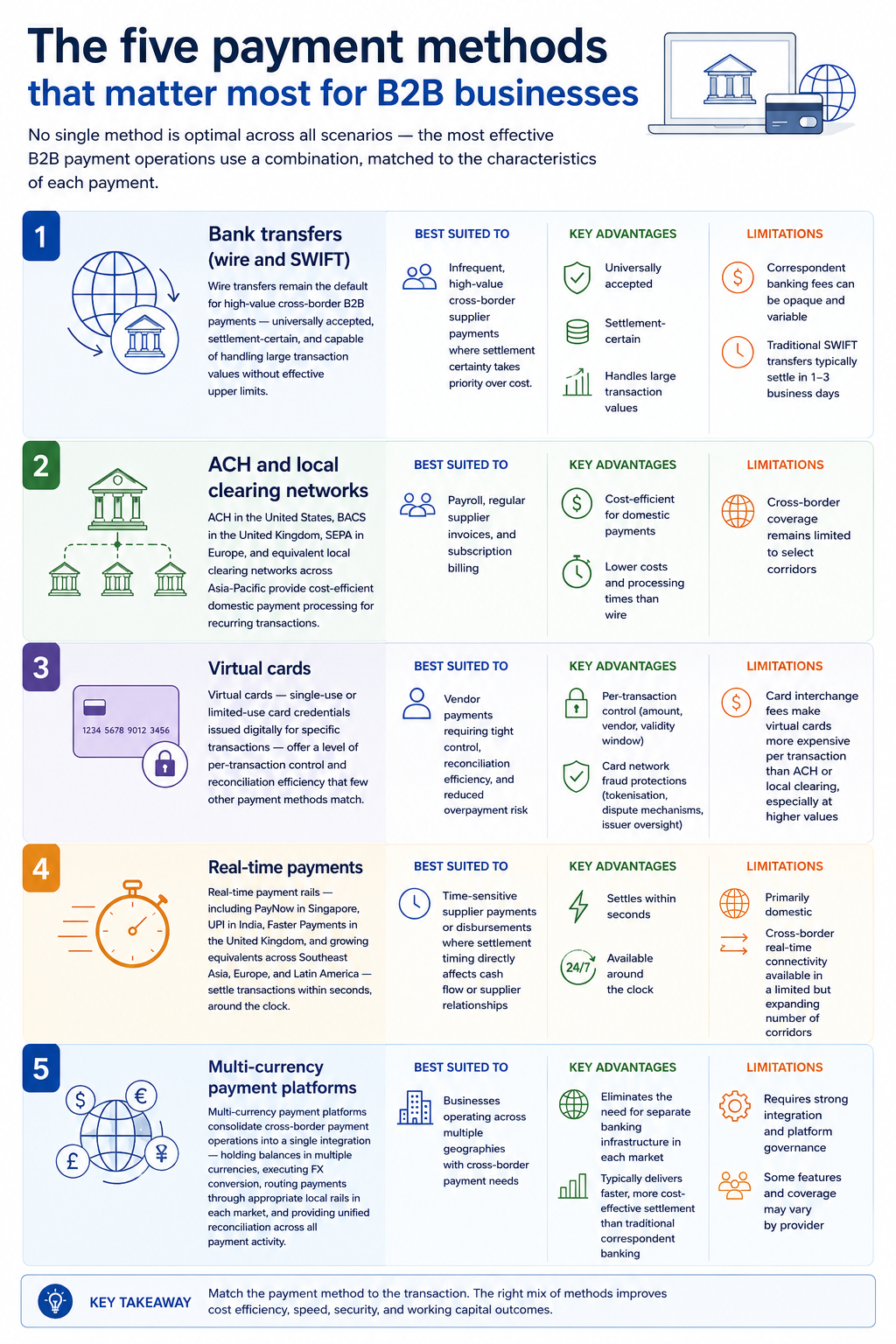

Most businesses set up a payment processing arrangement early and rarely revisit it — even as their transaction volumes, supplier relationships, and geographic footprint grow in ways the original setup was never designed to handle. Understanding who does what in a payment transaction, and which processing model fits your business, is the foundation for building payment operations that actually scale.

The key players in every payment transaction

Before evaluating payment methods or processors, it helps to understand the infrastructure that sits behind every transaction. Several distinct parties are involved each time a payment is made or received, and knowing what each one does makes it considerably easier to diagnose problems, negotiate pricing, and choose the right setup.

• Payment gateway

The payment gateway is the entry point for payment data. It securely captures a customer's payment information including card details, account credentials, or digital wallet data, and passes it to the payment processor for handling. In practice, the gateway is what enables a business to accept payments online or through a point-of-sale system. It also plays an important role in fraud prevention by encrypting payment data throughout the transaction process, so sensitive information is never exposed in transit.

• Payment processor

The payment processor is the operational engine behind the transaction. It takes the payment details from the gateway and routes them between the relevant banks while verifying the payment information, seeking authorisation from the customer's bank, and returning an approval or decline to the gateway in real time. Without the processor, no transaction completes.

• Merchant Account

A merchant account is a holding account for transaction funds. When a payment is approved, the funds do not move immediately to a business's operating account but are held in the merchant account during the settlement period, typically one to two business days, before being transferred through. Most businesses do not manage merchant accounts directly; payment service providers handle this on their behalf.

• Acquirer (acquiring bank)

The acquiring bank is the financial institution that processes card payments on behalf of the merchant. It acts as the receiving end of the card payment chain, accepting the transaction, holding the merchant account, and settling funds once the transaction clears. Crucially, the acquiring bank is what allows merchants to accept card payments from customers anywhere in the world without needing a direct relationship with every card-issuing bank that exists.

• Issuer (issuing bank)

The issuing bank is the institution that provided the customer's credit or debit card. It is the party that ultimately approves or declines a transaction, based on available funds, card validity, and fraud signals. This distinction matters operationally: when a transaction is declined, it is typically the issuing bank making that call and not the payment processor. This affects how the decline should be handled and whether a retry is appropriate.

Types of Payment Processors: Understanding the Models

The term "payment processor" covers several operating models, each affecting how a business accepts payments, manages its infrastructure, and controls costs.

Front-End vs. Back-End Processors

Front-end processors authorise transactions in real time, while back-end processors handle settlement by transferring funds after approval. Most businesses use payment service providers that combine both functions into a single platform.

Payment Service Providers vs. Dedicated Merchant Accounts

For most businesses, the key decision is choosing between a payment service provider (PSP) and a dedicated merchant account.

PSPs such as Stripe, PayPal and Airwallex bundle the gateway, processor and merchant account into one platform, offering fast onboarding and simple integration.

Dedicated merchant accounts require separate relationships with an acquiring bank and gateway provider. Although setup is more complex, businesses gain greater control over pricing, processing terms and direct negotiations as transaction volumes increase.

Choosing the right setup for your business

The right payment processing setup depends on your transaction profile: where your counterparties are located, what values and frequencies characterise your payment runs, how important settlement speed is relative to cost, and what level of control and reporting granularity your finance team requires.

For most B2B businesses, the practical starting point is a payment service provider for domestic and straightforward cross-border payments, supplemented by a multi-currency platform as international payment volumes grow. From there, evaluating whether a dedicated merchant account makes sense — based on transaction volume, corridor complexity, and the appetite for greater infrastructure control — is a natural next step as the business scales.

To get started and partner with a solutions provider that can help your business optimise payments and help you scale both locally and globally, open a SUNRATE account today or contact our sales team.

Share to

Most businesses set up a payment processing arrangement early and rarely revisit it — even as their transaction volumes, supplier relationships, and geographic footprint grow in ways the original setup was never designed to handle. Understanding who does what in a payment transaction, and which processing model fits your business, is the foundation for building […]

Payment infrastructure rarely becomes a concern until it starts slowing business growth. As B2B payments become more complex, businesses relying on legacy payment architectures risk delayed settlements, operational inefficiencies and rising compliance challenges. Identifying potential bottlenecks early is key to building a payment infrastructure that can scale with the business. Why Do Payment Bottlenecks Form? Payment bottlenecks are […]

Siloed payment operations rarely announce themselves. They reveal themselves gradually—in the time it takes to resolve a delayed payment, in the data that gets reported but never acted on, and in the moments when customers find themselves navigating your organisation instead of simply receiving answers. As global payment operations become increasingly complex, these inefficiencies become harder […]

We hope to use cookies to better understand your use of this website. This will help improve your future experience of accessing this website. For detailed information on the use of cookies and how to revoke or manage your consent, please refer to our < privacy policy >. If you click the confirmation button on the right, you will be deemed to have agreed to use cookies.