Payment infrastructure rarely becomes a concern until it starts slowing business growth. As B2B payments become more complex, businesses relying on legacy payment architectures risk delayed settlements, operational inefficiencies and rising compliance challenges. Identifying potential bottlenecks early is key to building a payment infrastructure that can scale with the business.

Why Do Payment Bottlenecks Form?

Payment bottlenecks are rarely caused by a single failure. More often, they stem from infrastructure decisions that worked at a smaller scale but struggle to support increasing transaction volumes, geographic expansion and regulatory complexity. Common causes include:

Single-rail dependency

• Heavy reliance on one correspondent bank or payment network

• Limited flexibility during outages or congestion

• Higher costs when alternative payment routes are unavailable

Fragmented payment systems

• Multiple providers added over time without integration

• Manual reconciliation between disconnected systems

• Inconsistent payment data and operational processes

Compliance processes that don't scale

• Manual AML and sanctions reviews

• Sequential compliance checks

• Slower payment processing as transaction volumes increase

The Shift Towards Multi-Rail Payment Architecture

One of the biggest structural shifts in B2B payment infrastructure is the move towards multi-rail payment architecture—operating across multiple payment networks, clearing systems and banking partners, with intelligent routing that selects the optimal payment path for each transaction. Rather than relying on a single payment rail, businesses can dynamically route payments based on:

• Cost – Select the most cost-effective payment route for each corridor

• Settlement speed – Optimise for faster payment delivery

• Network availability – Redirect payments during rail congestion or outages

• Operational resilience – Reduce reliance on any single banking partner or payment network

For businesses processing high transaction volumes across multiple markets, this level of flexibility is increasingly becoming a baseline requirement rather than a competitive differentiator.

The long-term advantage: A data flywheel

Every transaction processed through a multi-rail infrastructure generates valuable operational data that continuously improves future routing decisions, including:

• Settlement speeds by payment corridor

• Transaction failure rates

• Payment costs across different rails

• Compliance screening and exception rates

Reconciliation as a Hidden Bottleneck

Why It Matters

Reconciliation is one of the least visible payment infrastructure bottlenecks until it becomes critical. In fragmented payment environments, finance teams must match transactions across multiple systems, formats and settlement timelines—a labour-intensive process that becomes increasingly difficult to scale.

Over time, leading businesses are adopting real-time reconciliation to create a single view of payment status, settlement positions and cash flow across all payment rails and currencies. This enables finance teams to detect and resolve discrepancies as they occur, reducing operational risk and shifting from reactive problem-solving to proactive payment management.

The Benefits for High-Volume Businesses

For platforms and marketplaces managing large merchant or supplier networks, real-time reconciliation helps to:

• Reduce manual reconciliation effort

• Improve payment visibility across systems

• Identify discrepancies earlier

• Scale payment operations more efficiently

• Lower operational costs

Liquidity management as a structural advantage

Payment infrastructure bottlenecks are not only operational but also financial. Businesses operating across multiple currencies and settlement timelines are managing a complex, dynamic liquidity position that is difficult to optimise without real-time visibility into where cash is sitting, when it will settle, and what FX exposure it carries.

The emerging infrastructure model is one where liquidity management is embedded in the payment workflow rather than managed separately. Rather than monitoring cash positions through periodic treasury reports and making FX decisions manually, businesses are increasingly using payment platforms that surface real-time liquidity data and support automated or policy-driven FX execution. This reduces the working capital trapped in transit, shortens settlement cycles, and allows treasury teams to manage FX risk more precisely against defined policy parameters.

As settlement rails become faster, with instant or same-day settlement becoming standard across more corridors, the businesses best positioned to benefit are those whose liquidity infrastructure is already designed to operate in real time rather than on the batch settlement timelines that shaped treasury management practice for the past two decades.

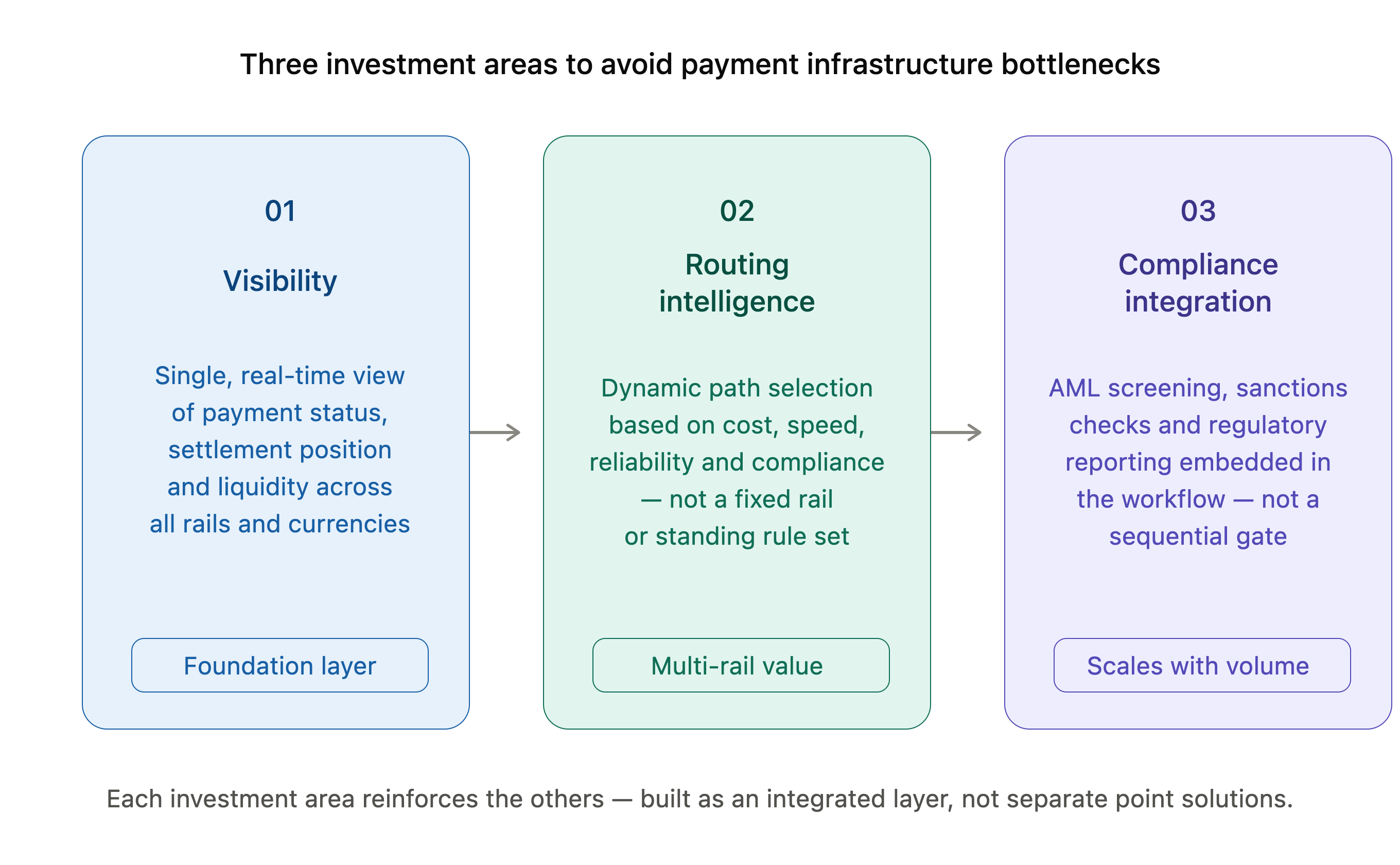

What infrastructure investment looks like in practice

Avoiding payment infrastructure bottlenecks does not require rebuilding from scratch. The businesses making the most meaningful progress are typically investing in three areas sequentially.

These are not independent investments. Each one reinforces the others, and the businesses building them as an integrated infrastructure layer, rather than as separate point solutions, are the ones finding that their payment infrastructure becomes a competitive asset rather than a constraint on growth.

To get started and partner with a solutions provider that can help your business optimise payments and help you scale both locally and globally, open a SUNRATE account today or contact our sales team.

Share to

Payment infrastructure rarely becomes a concern until it starts slowing business growth. As B2B payments become more complex, businesses relying on legacy payment architectures risk delayed settlements, operational inefficiencies and rising compliance challenges. Identifying potential bottlenecks early is key to building a payment infrastructure that can scale with the business. Why Do Payment Bottlenecks Form? Payment bottlenecks are […]

Siloed payment operations rarely announce themselves. They reveal themselves gradually—in the time it takes to resolve a delayed payment, in the data that gets reported but never acted on, and in the moments when customers find themselves navigating your organisation instead of simply receiving answers. As global payment operations become increasingly complex, these inefficiencies become harder […]

The corporate card used to be a static payment credential operating within a predetermined programme. AI is now transforming it into a programmable interface through which payment, risk, and spend decisions can be made in real time. For most of its history, the corporate card has been a relatively simple instrument. It carried a […]

We hope to use cookies to better understand your use of this website. This will help improve your future experience of accessing this website. For detailed information on the use of cookies and how to revoke or manage your consent, please refer to our < privacy policy >. If you click the confirmation button on the right, you will be deemed to have agreed to use cookies.