The build vs. buy debate has shaped enterprise technology decisions for decades. In B2B payments, it has never been more consequential or more misframed. The question finance and technology leaders are actually answering in 2026 is not "build or buy?" It is "what do we build, what do we buy, and how do we make them work together?"

Today, the landscape looks different. Cloud-native infrastructure, modular APIs, and a maturing ecosystem of specialist payment providers have created a middle ground — a hybrid model in which finance teams compose their payment stack from a combination of proprietary logic and third-party capability, rather than choosing between them entirely.

This shift is not ideological. It is pragmatic. Understanding why it is happening and what it means for how payment infrastructure decisions are made, is increasingly important for any business operating cross-border payment flows at scale.

Why neither extreme works at scale

The case for building comes down to control, which means proprietary infrastructure gives businesses ownership over the payment experience, the data it generates, and the competitive differentiation it can create.

The case for buying is equally clear: specialist providers have invested years and significant capital into compliance infrastructure, banking relationships, and payment network integrations that would take most businesses a decade to replicate.

The problem is that each approach, taken to its logical extreme, creates a different class of constraint.

Businesses that build everything face:

• The ongoing cost of maintaining infrastructure across a rapidly changing regulatory and technical landscape

• Internal engineering capacity that is expensive to build and difficult to retain, is consumed by every new payment corridor, regulatory change, and real-time rail that becomes table stakes in a new region

• Significant opportunity cost: engineering teams maintaining payment infrastructure are not building the product features that drive growth

Businesses that buy everything face:

• Dependency on a provider whose priorities may not align with their own, whether on pricing, feature development, corridor coverage, or data access

• Reduced negotiating leverage over time, as multi-year contracts and deep technical integration make switching costly

• Limited differentiation, because competitors using the same provider have access to the same capabilities

Neither constraint is fatal. But left unaddressed, both become ceilings on growth, on flexibility, and on the ability to compete on the quality of the payment experience itself.

The hybrid shift: what finance teams are actually doing

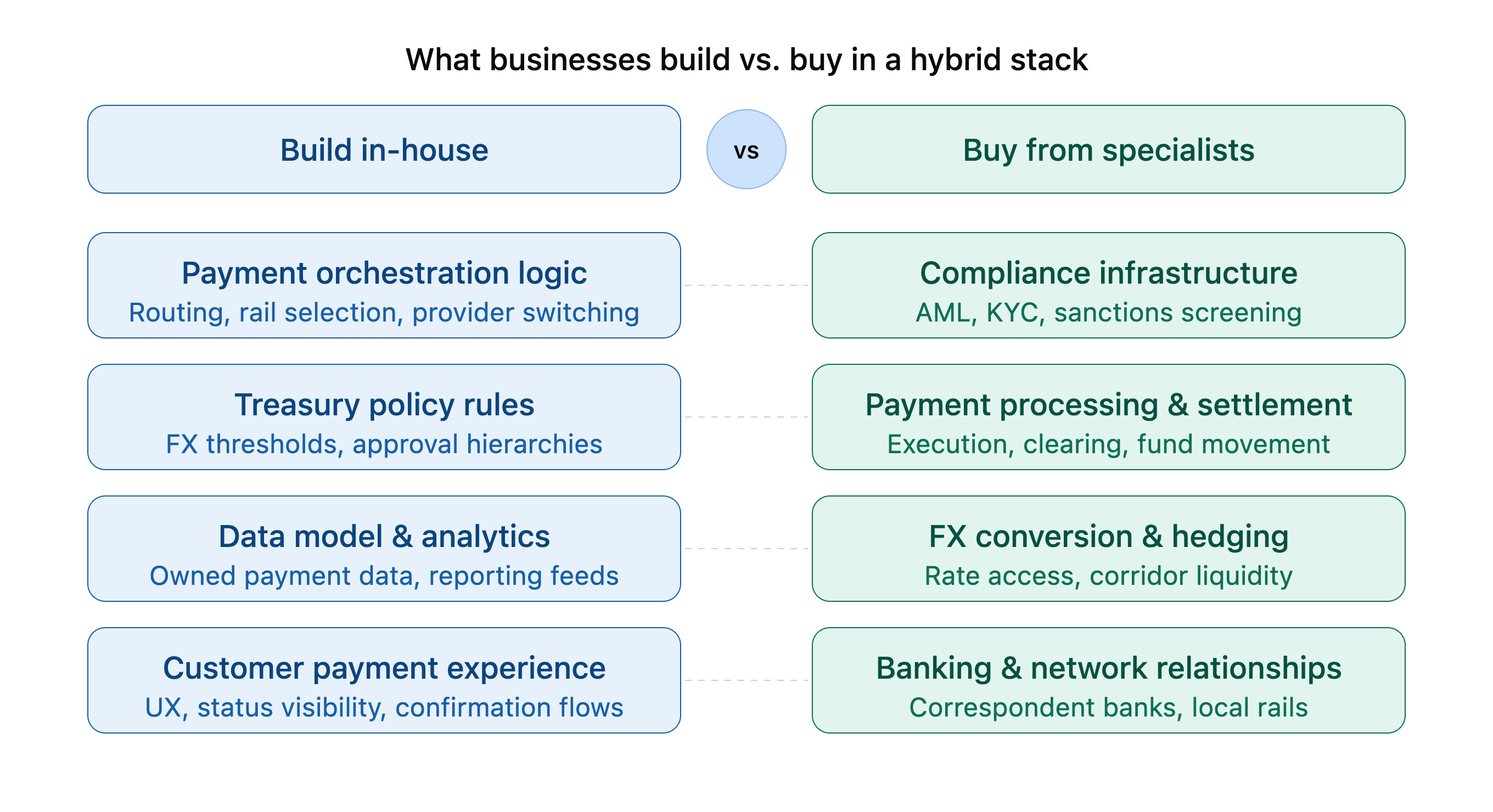

The pattern emerging across global B2B businesses is not a rejection of either approach — it is a more deliberate allocation of where each makes sense. The decisions that create the most differentiation, or that require the deepest integration with proprietary business logic, are increasingly built in-house. The decisions that require scale, regulatory expertise, or global network access are increasingly bought from specialist providers.

In payment operations, this typically resolves into a layered architecture. The orchestration layer, which is the logic that decides which payment method, which rail, and which provider handles a given transaction, is built or owned by the business. The execution layer, the actual payment processing, compliance screening, FX conversion, and settlement, is increasingly delivered by specialist providers through APIs.

This distinction matters because the orchestration layer is where the differentiation sits. A business that controls its own routing logic can optimise for cost, speed, and reliability simultaneously, switching between providers dynamically based on performance. A business that routes everything through a single provider is optimising only for simplicity.

The three forces driving hybrid adoption

1. Regulatory complexity that outpaces internal capacity

Cross-border payment compliance has grown significantly more complex. AML frameworks, sanctions lists, KYC requirements, and transaction reporting obligations differ across every jurisdiction and change frequently. Maintaining jurisdiction-specific compliance logic in-house, across every market a business operates in, requires a level of investment and specialist expertise that few businesses outside the largest financial institutions can sustain. Buying compliance infrastructure from providers with in-market regulatory relationships and dedicated compliance teams is increasingly the rational choice — even for businesses that build much of their payment stack in-house.

2. The API economy has lowered the cost of integration

The technical barrier to combining in-house and third-party infrastructure has fallen significantly. Modern payment providers expose their capabilities through well-documented APIs, making it possible to embed specialist functionality such as FX hedging, real-time settlement and virtual card issuance, into a proprietary orchestration layer without deep technical coupling. This means the hybrid model is now accessible to businesses with smaller engineering teams than it would have required even five years ago.

3. Data ownership is becoming a strategic priority

Payment data is one of the richest signals a global business generates, which include corridor performance, supplier payment behaviour, FX exposure patterns, cash flow timing. Businesses that route all their payments through a third-party platform may find that access to this data is limited, aggregated, or subject to the provider's terms. Building the orchestration layer in-house ensures that the data generated by payment decisions remains owned and accessible by the business, and can feed treasury management, financial planning, and operational decision-making rather than sitting in a provider's dashboard.

What the hybrid model demands

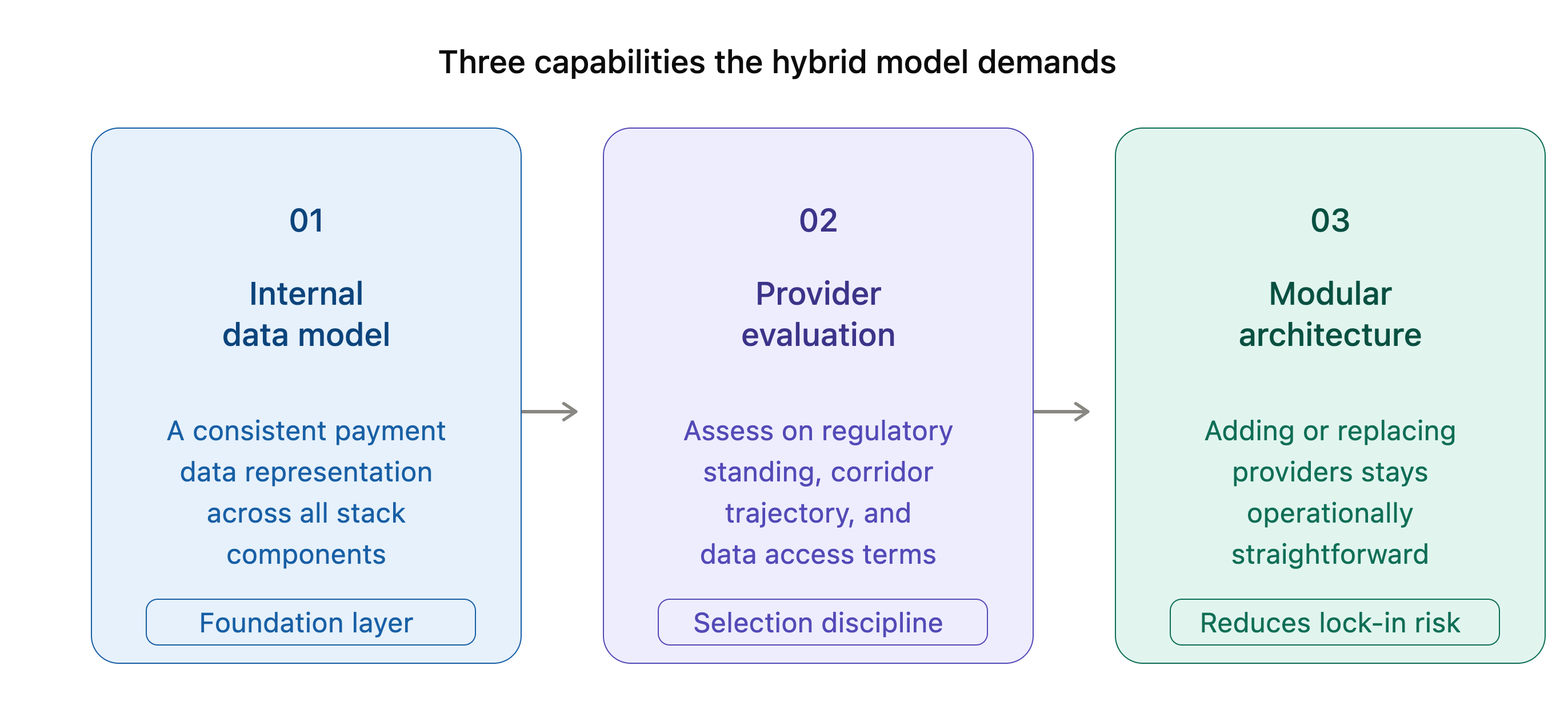

Adopting a hybrid approach is not without its own complexity. Composing a payment stack from multiple components — a proprietary orchestration layer, multiple specialist providers, a treasury management system, a compliance platform — creates integration overhead that a single-vendor approach avoids. The businesses navigating this well are those that invest in three foundational capabilities before adding complexity.

• The first is a clear internal data model. This is a consistent representation of payment data across all components of the stack, so that orchestration logic can operate on reliable inputs regardless of which provider or rail a transaction flows through.

• The second is robust provider evaluation, which is a systematic approach to assessing specialist providers not just on their current capabilities but on their regulatory standing, corridor coverage trajectory, and data access terms.

• The third is modular architecture, which refers to building the orchestration layer in a way that makes adding or replacing providers operationally straightforward, rather than deeply coupled integrations that make switching as painful as the situation they were designed to avoid.

The way forward

The hybrid model is not a temporary compromise between build and buy. It is the architecture that the evolution of payment infrastructure has made possible, and that the complexity of global payment operations increasingly demands.

Finance teams that treat payment infrastructure as a binary choice are leaving optionality on the table. The businesses building competitive advantage in cross-border payments are doing so by making deliberate, layered decisions about where to invest proprietary capability and where to leverage the depth of the specialist market — not by betting everything on either side of a debate that the market has already begun to resolve.

To get started and partner with a solutions provider that can help your business optimise payments and help you scale both locally and globally, open a SUNRATE account today or contact our sales team.

Share to

The build vs. buy debate has shaped enterprise technology decisions for decades. In B2B payments, it has never been more consequential or more misframed. The question finance and technology leaders are actually answering in 2026 is not “build or buy?” It is “what do we build, what do we buy, and how do we make them work together?” […]

Many early AI initiatives focus on automating individual steps within existing payment workflows, rather than reconsidering how the end-to-end process should operate. The result is faster execution of the same logic, not smarter outcomes. The next competitive advantage lies in building AI-first payment workflows — where AI supports or executes permitted routine decisions within defined […]

Most businesses set up a payment processing arrangement early and rarely revisit it — even as their transaction volumes, supplier relationships, and geographic footprint grow in ways the original setup was never designed to handle. Understanding who does what in a payment transaction, and which processing model fits your business, is the foundation for building […]

We hope to use cookies to better understand your use of this website. This will help improve your future experience of accessing this website. For detailed information on the use of cookies and how to revoke or manage your consent, please refer to our < privacy policy >. If you click the confirmation button on the right, you will be deemed to have agreed to use cookies.