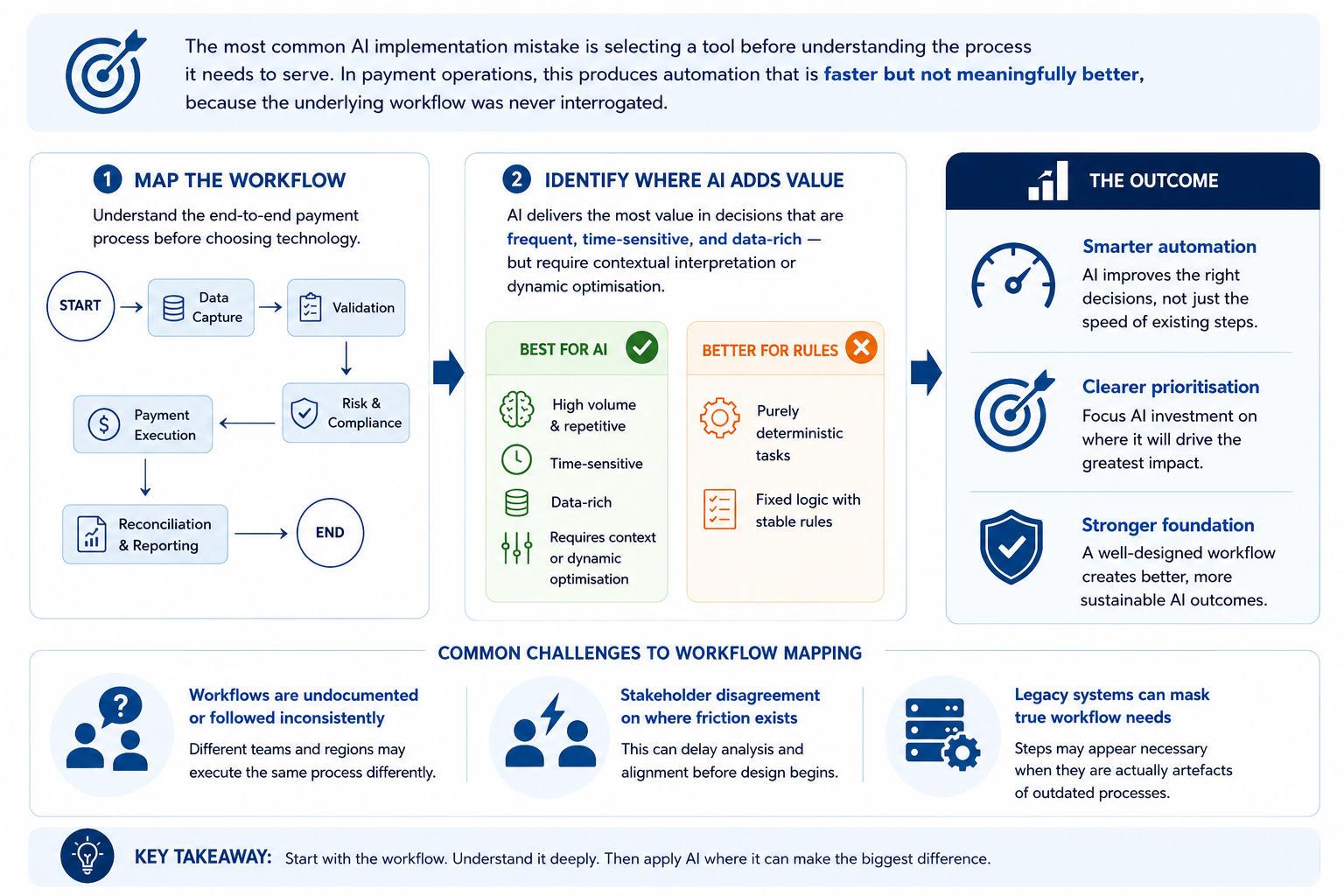

Many early AI initiatives focus on automating individual steps within existing payment workflows, rather than reconsidering how the end-to-end process should operate. The result is faster execution of the same logic, not smarter outcomes. The next competitive advantage lies in building AI-first payment workflows — where AI supports or executes permitted routine decisions within defined guardrails, while human teams retain responsibility for exceptions, high-risk cases, and material approvals.

AI-first payment workflows are only as strong as their exception logic. Automation changes the distribution of operational risk rather than eliminating it. Some risk concentrates in complex exceptions that fall outside the automation path; other risk emerges from incorrect automated decisions repeated at scale before they are detected.

Cross-border payments are particularly exception-prone — regulatory holds, incomplete beneficiary data, sanctions flags, and currency mismatches all generate cases that AI cannot confidently resolve. Designing for these edge cases with the same rigour applied to the straight-through path is what separates a genuinely resilient workflow from one that is merely efficient under normal conditions.

In practice, this means defining escalation rules, case ownership, and human review processes before the automation layer goes live and not as an afterthought once exception volumes become unmanageable. It also means ensuring that human review capacity scales alongside automation volume, so exception queues do not become the bottleneck that negates the efficiency gains elsewhere.

Data quality issues that seem minor in manual payment workflows can become significant failure points when AI is making decisions at scale. However, the challenge goes beyond clean data.

Effective AI payment workflows depend on a robust data architecture, including:

• A consistent internal data model

• Strong validation logic

• Source-system traceability

• Corridor-specific business rules

These are not simply prerequisites for AI—they are fundamental to how AI-first payment workflows operate

Beneficiary validation depends on far more than the payment corridor. AI must evaluate multiple variables simultaneously, including:

• Destination country

• Currency

• Payment rail

• Account type

• Transaction purpose

• Payment value

• Regulatory reporting requirements

Rather than applying a single validation standard, AI must dynamically determine the correct rule set for every transaction.

In many organisations, ERP systems, treasury platforms and payment systems operate independently, creating inconsistent data definitions.

Without:

• Source-system traceability, it becomes difficult to identify whether errors originate from the data, the AI model or system integrations.

• Closed feedback loops, payment failures are detected only after processing instead of being corrected at their source.

Businesses that treat data architecture as a one-off data cleansing exercise will find that AI exposes data quality issues faster than it resolves them. AI-first payment workflows require data architecture that is designed to scale—not simply data that is clean enough to begin with.

FX conversion and settlement routing decisions are made dozens or hundreds of times daily in a global business, yet most are still made manually or by default governed by standing treasury policies rather than real-time inputs. This is one of the most significant and under-optimised opportunities in AI-first payment design.

AI models that incorporate rate pattern analysis, volatility signals, and internal cash flow data can evaluate these inputs more quickly and consistently than a purely manual process, particularly at high transaction volumes. Over time, each AI-routed decision generates corridor performance data — FX slippage, settlement timing, failure rates — that improves the accuracy of subsequent decisions. The value compounds.

The design challenge is defining the optimisation criteria before the AI is deployed. Cost, speed, and predictability frequently pull in different directions, and without explicit priority settings aligned to treasury policy, the AI cannot resolve those trade-offs correctly. Data inputs must also be real-time and reliable — stale rate feeds undermine model accuracy precisely when accuracy matters most. And regulatory constraints on FX transactions vary by corridor, requiring the AI logic to be corridor-aware from the outset.

An AI payment workflow that performs well at launch is not guaranteed to perform well six months later. Models trained on historical data drift as fraud tactics shift, FX volatility changes, or regulatory requirements evolve. Without active monitoring, that drift may only become visible after it has already created operational, financial, or compliance impact.

AI models are constantly influenced by changing conditions, including:

• Evolving fraud tactics

• Fluctuating FX markets

• New regulatory requirements

• Changing payment patterns

Without continuous monitoring, performance degradation may go unnoticed until it has already affected payment operations.

Continuous monitoring should be designed into the workflow architecture from day one, rather than added after deployment. This includes:

• Establishing clear performance benchmarks before deployment

• Monitoring AI performance across multiple payment corridors

• Tracking outcomes across different currencies and transaction types

• Investing in the analytical infrastructure needed to support ongoing monitoring

• Assigning clear ownership for model performance over time

While these may seem straightforward, defining performance benchmarks before deployment is often one of the most difficult conversations—and one that many organisations postpone until problems emerge.

One of the biggest ongoing decisions is determining when to update a well-performing model versus maintaining its stability. There is no universal answer. What matters is that the decision is made deliberately, based on current performance data, rather than being delayed until model degradation forces corrective action.

Governance in an AI payment workflow is not a set of policies that sit alongside the technology. It is a set of structural constraints built into it — and it must be designed before scaling begins, not retrofitted after. Payment workflows carry direct authority to transfer funds. The consequences of an incorrectly permissioned AI action are financial and potentially irreversible, which makes the governance stakes higher here than in most other AI applications.

One of the most important design decisions is defining where AI authority ends and human oversight begins. Determining what AI can execute autonomously and what requires approval demands alignment across finance, compliance, legal and technology teams. In practice, reaching that agreement is often more challenging than the technical implementation itself.

Effective governance also depends on strong auditability. Decision logs should capture not only what the AI decided, but also the inputs, confidence signals and rule sets that informed the decision. Output-only logs provide little value during audits or incident investigations because they explain the outcome, but not how it was reached.

Human override and emergency suspension controls should be designed as independent safeguards rather than extensions of the AI system. These controls must be accessible to authorised personnel and thoroughly tested before the workflow goes live—not introduced only after an operational incident exposes the need for them.

Businesses that establish governance boundaries early are better positioned to:

• Satisfy regulatory and audit requirements

• Respond more effectively to operational incidents

• Expand AI decision-making authority safely as confidence in the system grows

Designing AI-first payment workflows begins with rethinking the workflow itself and not adding AI to existing processes and expecting different outcomes. The businesses that get this right will not just process payments faster. They will build operations with stronger control consistency, more informed FX decisions, and the governance foundations needed to absorb the next wave of AI capability as it arrives.

The competitive gap between those who redesign and those who automate the status quo will widen as AI continues to develop. The time to build the right foundations is before that gap becomes difficult to close.

To get started and partner with a solutions provider that can help your business optimise payments and help you scale both locally and globally, open a SUNRATE account today or contact our sales team.

Share to

Many early AI initiatives focus on automating individual steps within existing payment workflows, rather than reconsidering how the end-to-end process should operate. The result is faster execution of the same logic, not smarter outcomes. The next competitive advantage lies in building AI-first payment workflows — where AI supports or executes permitted routine decisions within defined […]

Most businesses set up a payment processing arrangement early and rarely revisit it — even as their transaction volumes, supplier relationships, and geographic footprint grow in ways the original setup was never designed to handle. Understanding who does what in a payment transaction, and which processing model fits your business, is the foundation for building […]

Payment infrastructure rarely becomes a concern until it starts slowing business growth. As B2B payments become more complex, businesses relying on legacy payment architectures risk delayed settlements, operational inefficiencies and rising compliance challenges. Identifying potential bottlenecks early is key to building a payment infrastructure that can scale with the business. Why Do Payment Bottlenecks Form? Payment bottlenecks are […]

We hope to use cookies to better understand your use of this website. This will help improve your future experience of accessing this website. For detailed information on the use of cookies and how to revoke or manage your consent, please refer to our < privacy policy >. If you click the confirmation button on the right, you will be deemed to have agreed to use cookies.